Economics > Econometrics

[Submitted on 8 Mar 2022 (v1), last revised 27 May 2024 (this version, v3)]

Title:On Robust Inference in Time Series Regression

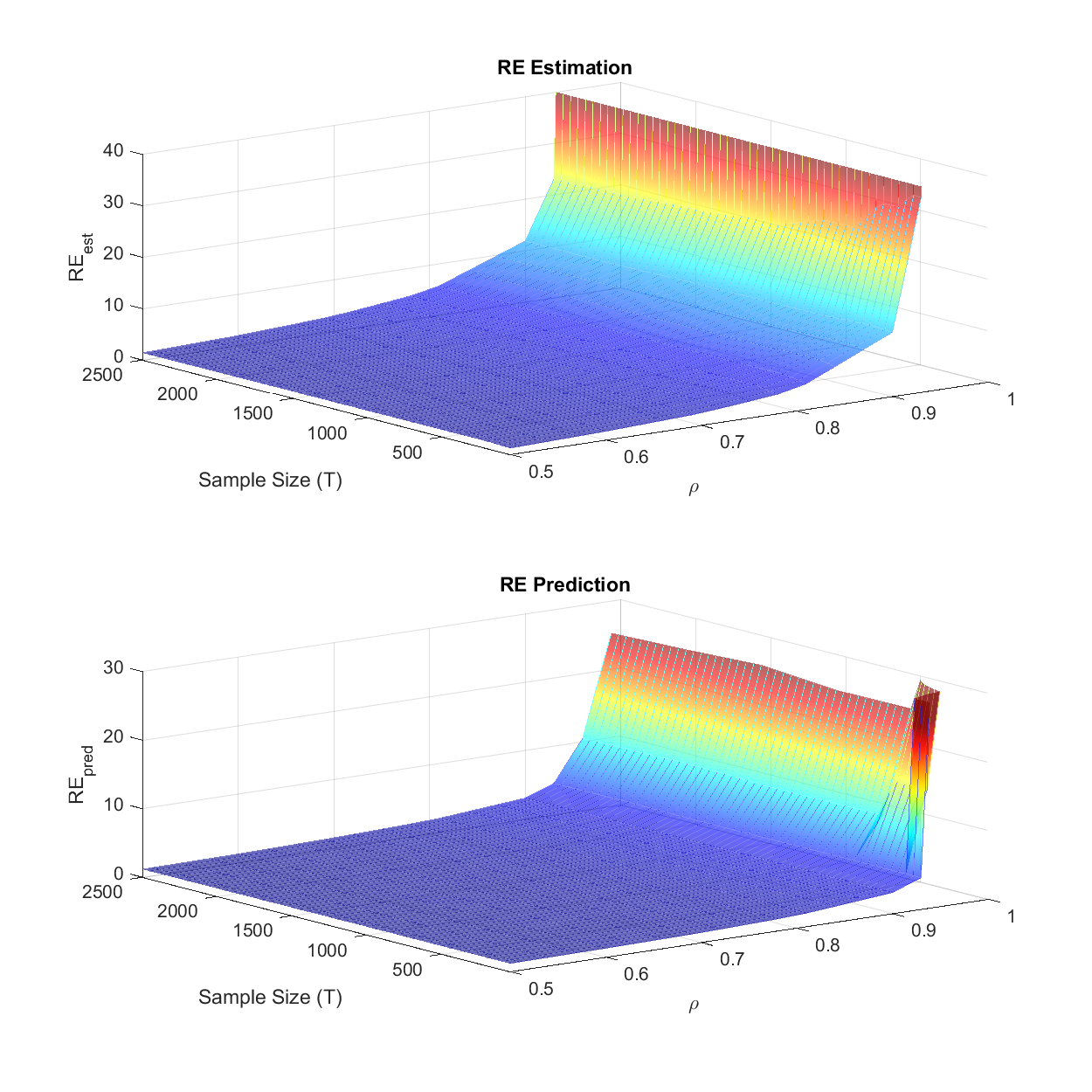

View PDF HTML (experimental)Abstract:Least squares regression with heteroskedasticity consistent standard errors ("OLS-HC regression") has proved very useful in cross section environments. However, several major difficulties, which are generally overlooked, must be confronted when transferring the HC technology to time series environments via heteroskedasticity and autocorrelation consistent standard errors ("OLS-HAC regression"). First, in plausible time-series environments, OLS parameter estimates can be inconsistent, so that OLS-HAC inference fails even asymptotically. Second, most economic time series have autocorrelation, which renders OLS parameter estimates inefficient. Third, autocorrelation similarly renders conditional predictions based on OLS parameter estimates inefficient. Finally, the structure of popular HAC covariance matrix estimators is ill-suited for capturing the autoregressive autocorrelation typically present in economic time series, which produces large size distortions and reduced power in HAC-based hypothesis testing, in all but the largest samples. We show that all four problems are largely avoided by the use of a simple and easily-implemented dynamic regression procedure, which we call DURBIN. We demonstrate the advantages of DURBIN with detailed simulations covering a range of practical issues.

Submission history

From: Francis Diebold [view email][v1] Tue, 8 Mar 2022 13:49:10 UTC (2,881 KB)

[v2] Wed, 18 Oct 2023 14:36:51 UTC (7,851 KB)

[v3] Mon, 27 May 2024 20:02:49 UTC (8,279 KB)

Ancillary-file links:

Ancillary files (details):

- OLS.m

- a1_Simulate_Size_MSE_ARMA.m

- a1_Simulate_Size_MSE_VAR.m

- a1_Simulate_Size_MSE_lagsX.m

- a4_PredAcc_Table.m

- a5_RE_Figure.m

- a6_Power_Figures_Data_AR.m

- a6_Power_Figures_Data_ARMA.m

- a6_Power_Figures_Data_MA.m

- a6_Power_Figures_Data_VAR.m

- a6_Power_Figures_Data_lagsX.m

- a7_Power_Figure_fixedT_AR.m

- a7_Power_Figure_fixedT_ARMA.m

- a7_Power_Figure_fixedT_VAR.m

- a8_Power_Figure_fixedRho_ARMA.m

- a_Readme.txt

- cosine_weight.m

- formatted_tables/Table_MSE_Size_ARMA.xlsx

- formatted_tables/Table_MSE_Size_VAR.xlsx

- formatted_tables/Table_MSE_Size_lagsXY.xlsx

- formatted_tables/Table_prediction.xlsx

- genData_n_Test_ARMA.m

- genData_n_Test_VAR.m

- genData_n_Test_lagsX.m

- genData_n_Test_t_errors.m

- hac.m

- omega_hat_cos.m

- perform_test.m

- plots/Power_fixedRho_ARMA_BIC_paper.png

- plots/Power_fixedRho_AR_BIC_paper.png

- plots/Power_fixedRho_MA_BIC_paper.png

- plots/Power_fixedT_ARMA_BIC_paper.png

- plots/Power_fixedT_AR_BIC_paper_ap11.png

- plots/Power_fixedT_MA_BIC_paper.png

- plots/Power_fixedT_VAR_1_3_ap11.png

- plots/Power_fixedT_VAR_2_4_ap11.png

- plots/RE_AR_BIC.png

- predictiveAcc.m

- tables/Figure_PowerFixedPhi_VAR.mat

- tables/Figure_PowerFixedRho_AR.mat

- tables/Figure_PowerFixedRho_ARMA.mat

- tables/Figure_PowerFixedRho_MA.mat

- tables/Figure_PowerFixedRho_lags.mat

- tables/Figure_PowerFixedT_AR.mat

- tables/Figure_PowerFixedT_ARMA.mat

- tables/Figure_PowerFixedT_MA.mat

- tables/Figure_PowerFixedT_VAR.mat

- tables/Figure_PowerFixedT_lags.mat

- tables/Figure_RE_Data.mat

- tables/Tables_ARMA_MSE_Size.mat

- tables/Tables_AR_MSE_Size.mat

- tables/Tables_MA_MSE_Size.mat

- tables/Tables_PredAcc.mat

- tables/Tables_VAR_MSE_Size.mat

- tables/Tables_lagsX_MSE_Size.mat

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Current browse context:

econ.EM

References & Citations

Bookmark

Bibliographic and Citation Tools

Bibliographic Explorer (What is the Explorer?)

Connected Papers (What is Connected Papers?)

Litmaps (What is Litmaps?)

scite Smart Citations (What are Smart Citations?)

Code, Data and Media Associated with this Article

alphaXiv (What is alphaXiv?)

CatalyzeX Code Finder for Papers (What is CatalyzeX?)

DagsHub (What is DagsHub?)

Gotit.pub (What is GotitPub?)

Hugging Face (What is Huggingface?)

Papers with Code (What is Papers with Code?)

ScienceCast (What is ScienceCast?)

Demos

Recommenders and Search Tools

Influence Flower (What are Influence Flowers?)

CORE Recommender (What is CORE?)

arXivLabs: experimental projects with community collaborators

arXivLabs is a framework that allows collaborators to develop and share new arXiv features directly on our website.

Both individuals and organizations that work with arXivLabs have embraced and accepted our values of openness, community, excellence, and user data privacy. arXiv is committed to these values and only works with partners that adhere to them.

Have an idea for a project that will add value for arXiv's community? Learn more about arXivLabs.